In January 2026, a Boston Consulting Group report formally described AI assistants as “insurers’ new front door”, the primary gateway through which millions of American consumers now first encounter, compare, and purchase insurance products. That framing would have seemed far-fetched even three years ago.

Today, it defines the competitive reality facing every licensed broker, independent agent, and digital distribution platform operating in the U.S. market. The rise of the AI insurance agent is no longer a future scenario reserved for industry white papers. It is a live, commercial, and increasingly regulated phenomenon that is reordering how coverage gets explained, quoted, and sold across all major lines of insurance.

What makes 2026 a genuinely critical inflection point is not simply the proliferation of chatbot interfaces. It is the simultaneous surge in agentic AI capabilities and the sharpening of regulatory scrutiny from state insurance departments and the National Association of Insurance Commissioners.

As of March 2026, the NAIC’s Big Data and Artificial Intelligence Working Group is actively piloting an AI Systems Evaluation Tool across 12 participating states, a structured examination instrument designed to assess how insurers deploy AI in underwriting, pricing, marketing, and customer-facing advisory functions.

The pilot is expected to conclude in September 2026, with formal adoption anticipated at the Fall National Meeting. That timeline matters enormously, because the rules governing what an AI insurance agent can lawfully do, and who bears liability when it gets something wrong, are being written right now, in real time.

Against that backdrop, the question that consumers, regulators, and industry professionals are asking with increasing urgency is straightforward: can a chatbot give better insurance advice than a licensed human broker? The honest answer requires separating several distinct dimensions, data processing speed, recommendation accuracy, regulatory standing, fiduciary accountability, and the handling of complex, high-stakes coverage scenarios.

Each dimension tells a different story, and the cumulative picture is more nuanced than either the technology optimists or the human-first traditionalists tend to acknowledge. A balanced assessment demands real accuracy analysis, not marketing claims. That is precisely what follows.

What an AI Insurance Agent Actually Does in 2026

The term “AI insurance agent” covers a wide spectrum of tools. At the lower end sit rule-based chatbots that answer FAQs about deductibles and policy renewal dates, essentially digital filing cabinets with a conversational interface.

At the more sophisticated end, which is where the market is rapidly moving in 2026, sit agentic AI systems capable of end-to-end insurance transactions: collecting risk profile data, cross-referencing carrier offerings in real time, generating personalized quotes, flagging coverage gaps, and in some cases initiating policy issuance without any human intervention.

The distinction between these tiers is consequential. A simple chatbot handling First Notice of Loss (FNOL) reporting or policy FAQs operates with low advisory risk. An agentic system that recommends a specific liability limit to a small business owner or advises a senior consumer on whether a Medicare Advantage plan fits their chronic care needs is performing a fundamentally different function, one that, when performed by a licensed human, carries explicit legal duties under state insurance law.

According to a December 2025 analysis by Roots.ai, analysts project that by late 2026, more than 35% of U.S. insurers will deploy AI agents across at least three core operational functions, including customer-facing advisory interactions. The scale of adoption is not in question.

What remains contested is whether these systems are delivering genuinely accurate, contextually appropriate, and legally defensible guidance, or whether they are producing confident-sounding outputs that fall short of the standard a licensed professional would be held to.

Regulatory and Market Shifts in Q1 2026

The regulatory environment surrounding AI advisory tools in insurance has moved with unusual speed in the opening months of 2026. Several developments are reshaping both what is legally permissible and what carries enforcement risk.

NAIC AI Evaluation Tool Pilot (January to September 2026)

The most operationally significant development is the NAIC’s launch of its multistate AI Evaluation Tool pilot, running from January through September 2026. Twelve states are currently participating, with the tool designed to function as a structured examination instrument for market conduct and financial reviews.

The NAIC’s stated position is unambiguous: existing state insurance laws apply regardless of whether decisions are made by humans, algorithms, or third-party vendors. That principle has immediate implications for any insurer or insurtech platform deploying an AI insurance agent in a consumer-facing advisory capacity.

Colorado AI Act Takes Effect (February 1, 2026)

Colorado’s Artificial Intelligence Act, passed in May 2024, formally took effect on February 1, 2026, making Colorado the first U.S. state with a comprehensive framework governing high-risk AI systems, including those used in insurance underwriting and customer advisory functions.

The Act requires consumer disclosure, bias prevention protocols, and board-approved risk management policies for insurers deploying AI in consequential decisions. Virginia enacted closely mirroring legislation (HB 2094) in the same legislative cycle. Insurers operating across multiple states now face a patchwork of requirements that will grow more complex as additional state legislatures act.

NAIC Model Bulletin Adoption Reaches 24 States

By March 2026, approximately 24 states had adopted the NAIC’s December 2023 Model Bulletin on the Use of Artificial Intelligence Systems by Insurers, which requires a documented AI Systems Program aligned with the NAIC’s FACTS principles (Fairness, Accountability, Compliance, Transparency, and Security).

A model law governing third-party AI vendors, which would directly affect insurtech platforms supplying AI advisory tools to carriers, is anticipated for introduction in 2026, potentially including formal licensing requirements for those vendors.

Federal Executive Order Tension

The regulatory picture was complicated in early 2026 when President Trump signed an executive order establishing a single national AI regulation framework, which the NAIC publicly characterized as introducing legal uncertainty and undermining state-based consumer protections built over 150 years.

The NAIC expressed confidence that state commissioners retain authority to coordinate AI supervision consistent with federal law, but the tension between federal preemption and state regulatory primacy remains an active and unresolved legal question heading into the second half of 2026.

AI vs. Human Insurance Agent: Head-to-Head Accuracy Analysis

The most important question for consumers is not whether AI insurance agents exist, but whether their recommendations are accurate enough to be trusted with coverage decisions that carry genuine financial consequences.

Where AI Systems Demonstrably Outperform Human Agents

On tasks that are data-intensive, repeatable, and well-defined by structured rules, AI advisory tools show measurable advantages. Processing large volumes of risk variables simultaneously, cross-referencing carrier rate filings in real time, detecting inconsistencies in application data, and identifying obvious coverage gaps in standardized personal lines products are areas where well-trained AI models exceed the practical capacity of any individual human agent working within a normal appointment window.

In a February 2026 BCG report, AI assistants were credited with accelerating the discovery, comparison, and purchase phases of insurance distribution, particularly for commoditized personal lines products like auto, renters, and standard homeowners policies.

Tuio, an AI-driven home insurance platform, reported in early 2026 that 97% of its customers complete the contracting process without human assistance, a figure that reflects both the simplicity of standard product designs and the maturity of AI-driven quoting interfaces.

A 2025 industry survey referenced by AgentSync found that the global AI in insurance market, valued at $4.59 billion in 2022, is projected to reach $79.86 billion by 2032, growing at over 33% annually. That trajectory reflects genuine market confidence in AI’s operational value, even as regulatory frameworks struggle to keep pace.

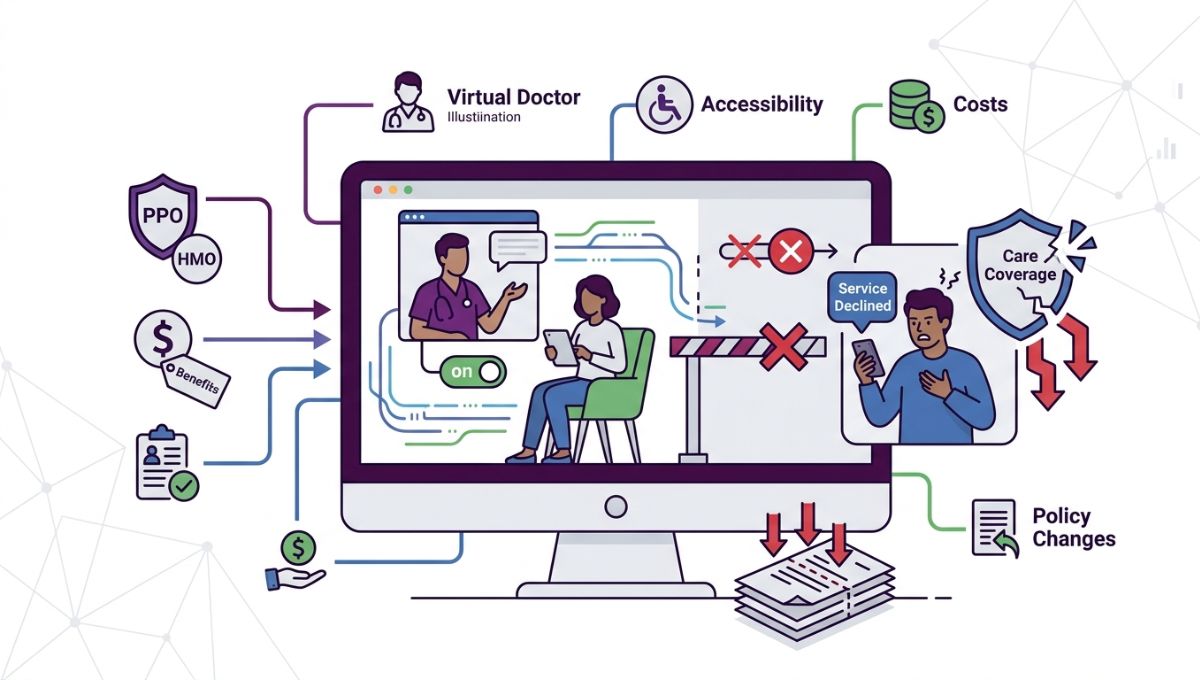

Where AI Recommendation Accuracy Falls Short

The picture changes substantially when the advisory scenario involves product complexity, regulatory nuance, or significant financial stakes. A January 2026 analysis published through Stanford Report found that AI-driven insurance decision systems risk amplifying existing algorithmic flaws, particularly in health insurance contexts where coverage denials, prior authorization decisions, and plan selection recommendations carry high consumer impact.

The Fenwick analysis of the NAIC’s 2025 survey data is particularly striking: nearly one-third of health insurers still do not regularly test their AI models for bias or discrimination, even though the NAIC Model Bulletin explicitly recommends such practices. An AI insurance agent built on an undertested model is, by definition, producing recommendations whose accuracy profile is unknown to both the insurer and the consumer it is advising.

In the specialized domain of endorsement interpretation, which is critical to determining whether a policy actually covers a claimed loss, no major AI platform in 2026 fully automates the analysis without human review. A comprehensive assessment of COI tracking platforms (BCS, Jones, illumend, TrustLayer, myCOI, Certificial) found that every major vendor still routes complex endorsements to human reviewers, and that vendor accuracy claims of 99.9% or 99.5% are not standardized and cannot be directly compared across platforms. Coverage gaps in complex commercial lines, surplus lines products, or policies with significant manuscript language remain outside the reliable advisory range of current AI systems.

The human-in-the-loop principle is not merely a regulatory preference, it reflects a genuine technical limitation. According to a January 2026 report from FinTech Global, AI can suggest decisions on risk appetite and compliance, but human validation remains necessary to ensure adherence to underwriting standards and regulatory requirements. Errors in coverage terms, premiums, or sublimits identified after policy issuance can produce claim disputes that cost policyholders far more than the advisory fee they saved by bypassing a human broker.

The Fiduciary and Suitability Gap: What No AI Holds

Perhaps the most underappreciated distinction between an AI insurance agent and a licensed human broker is the legal accountability framework that governs the human and, critically, does not yet govern the machine in any consistent or enforceable way.

Suitability, Best Interest, and Fiduciary Standards

Licensed insurance producers in the United States operate under a legally established framework of professional duties. The suitability standard, which governs most insurance product sales, requires that a producer not recommend a product that falls outside a client’s stated objectives and financial means.

The best interest standard, codified through the NAIC’s 2020 update to its Suitability in Annuity Transactions Model Regulation, goes further: it requires that the producer’s recommendation reflect the consumer’s best interest without placing the agent’s or insurer’s financial interests ahead of the client’s. For certain annuity sales and, in states like California and under DOL rules, for fiduciary-classified activities, an even stricter fiduciary standard applies

An AI insurance agent, regardless of how sophisticated its recommendation engine, does not currently hold a state insurance producer license in any U.S. jurisdiction. The insurer or insurtech platform behind the tool is responsible for any regulatory violations the AI system produces, but that accountability runs through the entity’s licensing framework, not through a direct fiduciary relationship with the consumer. When an AI recommends a policy that turns out to be unsuitable for a consumer’s specific health, liability, or property situation, the legal remedy pathways are far less clear than they would be in a dispute with a licensed broker of record.

Commission Transparency and Conflict of Interest

Licensed brokers are subject to disclosure requirements regarding compensation, commissions, and conflicts of interest, requirements that vary by state but reflect a consistent regulatory principle: consumers have a right to understand the financial incentives shaping the advice they receive.

AI insurance advisory tools embedded in carrier websites or insurtech platforms often reflect the carrier’s own product portfolio, a built-in structural preference that is rarely disclosed with the same explicitness a licensed independent broker would be required to provide. Where these tools exist within aggregator or comparison platforms, the conflict of interest is less direct, but the question of commission transparency remains relevant wherever an AI system presents one coverage option as superior to another.

Understanding how insurance companies calculate risk and structure premiums is foundational to evaluating whether any advisory recommendation, human or AI, genuinely reflects a consumer’s risk profile.

Comparing AI and Human Advisory Performance Across Key Scenarios

| Advisory Scenario | AI Insurance Agent Performance | Licensed Human Broker Performance |

|---|---|---|

| Standard personal auto quote (state minimums) | Excellent, fast, accurate, multi-carrier | Good, may be slower, similarly accurate |

| Health plan selection (ACA marketplace) | Moderate, handles plan comparisons; limited on subsidy nuance | Strong, navigates subsidy calculations, special enrollment rules |

| Medicare Advantage plan recommendation | Weak, high error risk on chronic care, drug formulary matching | Strong, fiduciary duty in many states; deep plan knowledge |

| Commercial general liability for a small business | Poor, endorsement and industry-specific nuances exceed AI capability | Strong, can access surplus lines markets, negotiate terms |

| Life insurance needs analysis | Moderate, strong on term quoting; weak on complex whole/UL structures | Strong, suitability analysis, income replacement modeling |

| Annuity recommendation | Very poor, fiduciary standard legally required; no AI holds this | Required, best interest standard applies by NAIC model regulation |

| Claims advocacy after denial | Not applicable, AI cannot advocate or negotiate claims | Essential, broker of record has standing to engage insurer |

AI Adoption Rates by Insurance Sector (2025 NAIC Survey Data)

| Insurance Line | AI Adoption Rate (Current or Planned) | Regular Bias Testing Conducted |

|---|---|---|

| Health Insurance | 92% | Approximately 67% |

| Auto Insurance | 88% | Not separately reported |

| Homeowners Insurance | 70% | Not separately reported |

| Life Insurance | 58% | Not separately reported |

Source: NAIC Big Data and Artificial Intelligence Working Group surveys, reported 2025 (Fenwick AI Regulation Tracker).

The Hybrid Model: Where the Industry Is Actually Going

The binary framing of AI versus human agent is, in practice, not how most serious insurers or distribution platforms are positioning themselves for 2026 and beyond. The prevailing strategic direction among carriers, MGAs, and independent distribution groups is a hybrid model, one in which AI handles the high-volume, data-structured, and time-sensitive functions, while human professionals concentrate on complex advisory work, claims advocacy, relationship management, and regulatory compliance oversight.

Industry reporting from mid-2025 captured the dynamic precisely: agents are moving from transaction processors to trusted advisors, focusing on complex case guidance, relationship-building, and long-term strategic planning, with AI handling the administrative and preliminary analysis layers that once consumed most of a producer’s working day. A regional insurer that implemented a hybrid AI framework in late 2024 reportedly reduced claims processing time by 40% while improving customer satisfaction, by requiring human review for decisions involving claims over $50,000 and flagging AI recommendations for escalation whenever confidence scores dropped below 85%.

For consumers, the hybrid model has practical implications. The initial quoting, comparison, and enrollment experience may be entirely AI-driven, faster and more available than a broker appointment, particularly for straightforward personal lines coverage. But when coverage decisions involve significant assets, chronic health conditions, business liability exposure, or complex annuity and life products, the suitability and fiduciary protections that only a licensed human provides are not merely procedural courtesies. They are substantive legal safeguards.

Consumers researching health plan options specifically benefit from understanding how various plan architectures differ. A thorough review of PPO, HMO, and EPO structures helps clarify what AI comparison tools are actually comparing when they generate side-by-side health plan recommendations. Similarly, consumers who understand the distinction between short-term and long-term health insurance designs are better positioned to evaluate whether an AI-generated recommendation is actually appropriate for their coverage timeline.

State Licensing for AI: The Unresolved Legal Question

One of the most consequential unresolved questions in the 2026 insurance regulatory environment is whether, or under what conditions, an AI system performing insurance advisory functions requires a state insurance producer license, or whether the licensing obligation rests exclusively with the insurer or platform deploying the system.

Current NAIC guidance is that existing state insurance laws apply regardless of whether decisions are made by humans, algorithms, or third-party vendors. This means the licensed insurer is responsible for regulatory compliance, accurate consumer disclosures, and non-discriminatory outcomes, even when an AI system produces the recommendation. The agent of record in a policy transaction remains a licensed human entity or a licensed corporate producer. The AI is treated, legally, as a tool used by that licensed entity.

The anticipated 2026 model law on third-party data and model oversight, currently under development by the NAIC’s working group, is expected to introduce more formal due diligence requirements, contractual controls, and potentially licensing obligations for AI vendors supplying advisory tools to the insurance sector. Until that framework is finalized, the absence of direct licensing requirements for AI advisory systems creates a structural accountability gap that benefits neither consumers nor the broader regulatory framework.

Understanding how the broader landscape of AI applications in health insurance has evolved, including its role in coverage decisions and denials, provides important context for this regulatory debate. The future of home insurance, similarly, is being shaped by AI-driven underwriting and risk assessment tools that are already influencing how coverage is priced and structured at the individual property level.

AI Recommendation Accuracy: State-by-State Regulatory Variability

Because insurance regulation in the United States is inherently state-based, the reliability and regulatory compliance of AI insurance advisory tools varies materially depending on where a consumer is located.

A consumer in Colorado, where the AI Act took effect in February 2026, theoretically benefits from mandatory disclosure, bias prevention, and board-approved risk management requirements before any AI system influences their insurance coverage. A consumer in a state that has not yet adopted the NAIC Model Bulletin has no equivalent protection.

| State Category | NAIC Model Bulletin Adopted | State-Specific AI Law | AI Evaluation Tool Pilot Participant |

|---|---|---|---|

| Early adopters (e.g., CO, CA, NY) | Yes | Yes (varies) | Likely |

| Mid-tier adopters (~24 states total) | Yes | Limited | Possible |

| Non-adopters (~26 states + territories) | No | No | Unknown |

Source: Crowell & Moring, March 2026; Fenwick, February 2026.

This regulatory patchwork means that the level of consumer protection embedded in an AI insurance agent interaction is, in material ways, a function of state residency, a fact that most consumers are entirely unaware of when they interact with a chatbot quoting tool.

Liability When AI Gets It Wrong

The question of who bears liability when an AI insurance agent provides inaccurate, incomplete, or unsuitable advice is not merely academic. It is a live legal issue that has produced real disputes and is generating significant attention from errors and omissions insurers, who are increasingly introducing exclusions for AI-related advisory failures.

W.R. Berkley introduced an absolute AI exclusion for D&O, E&O, and Fiduciary Liability policies, eliminating coverage for claims arising from the use or deployment of AI, including chatbot communications and AI-driven coverage recommendations. Hamilton Insurance Group introduced a Generative AI Exclusion removing coverage for claims from systems producing content in response to user prompts.

The Air Canada chatbot case of 2024, in which a carrier unsuccessfully attempted to disclaim responsibility for false information its chatbot provided to a customer, established a precedent that AI outputs carrying financial consequences are attributable to the entity deploying the system, not the technology itself.

For consumers, this liability landscape has a practical implication: when an AI insurance agent recommends a coverage structure that turns out to be inadequate at the time of a loss, the legal and financial remedy path is substantially more complex than it would be with a licensed broker who carries professional E&O coverage, holds a fiduciary or suitability obligation, and is subject to state insurance department complaint and enforcement mechanisms. Hidden dangers of underinsurance, many of which arise precisely from advisory gaps, carry real financial consequences that no algorithm can resolve after the fact.

Concluding Perspective: Informed Consumers in an AI-Augmented Insurance Market

The rise of the AI insurance agent represents one of the most substantive transformations in insurance distribution since the emergence of direct-to-consumer carriers in the 1990s. The efficiency gains are real. The data-processing advantages are demonstrable.

And for straightforward, standardized coverage needs, a state-required auto policy, a basic renters plan, a term life quote for a healthy applicant in a standard risk class, an AI-driven platform can deliver a faster, multi-carrier comparison than most broker appointments can match on speed alone.

But the characteristics that define consequential insurance decisions, complexity, regulatory nuance, product suitability, claims advocacy, and legal accountability, remain areas where licensed human professionals operate with authority and legal standing that no AI system currently possesses in the U.S. regulatory environment. A chatbot does not hold a fiduciary obligation. It cannot be the agent of record on a policy. It cannot advocate with an insurer on a disputed claim.

And in 2026, it cannot be licensed as a producer in any U.S. state, meaning the legal responsibilities that would protect a consumer in an advisory relationship with a human flow through the insurer or platform deploying the AI, not through a direct professional obligation to the policyholder.

The most important development to watch in the second half of 2026 is the NAIC’s AI Evaluation Tool pilot conclusion and the anticipated model law on third-party AI vendors. If that model law introduces direct accountability standards for AI advisory systems, including disclosure, bias testing, and performance audit requirements, it would represent a significant step toward closing the accountability gap that currently exists between AI-driven and human-delivered insurance advice.

For consumers navigating this environment, the practical guidance is grounded in the nature of the coverage decision at hand. For standard personal lines products with clear coverage terms, AI comparison tools can accelerate the quoting process and support informed comparison.

For complex decisions involving significant asset protection, health-specific coverage design, annuity products, business liability, or any scenario where a coverage gap would produce a material financial loss, the combination of an AI-assisted quoting process followed by review with a licensed professional remains the highest-confidence path to appropriate coverage.

Using neutral quote-comparison platforms to gather baseline market data, then consulting a licensed advisor for suitability confirmation, reflects the hybrid model that the industry itself is converging on for good reason.

The insurance market of 2026 is not a choice between a chatbot and a broker. It is a market in which informed consumers can use both, strategically, with a clear understanding of what each does well and where each falls short.

Frequently Asked Questions

1. What exactly is an AI insurance agent?

An AI insurance agent is a technology system, ranging from a conversational chatbot to a sophisticated agentic AI platform, that performs insurance advisory, quoting, or transactional functions traditionally handled by licensed human producers. In 2026, these systems span a wide capability range, from basic FAQ tools to end-to-end platforms that quote, compare, and in some cases bind policies without human intervention. No AI system currently holds a state insurance producer license in any U.S. jurisdiction.

2. Can an AI insurance agent legally give personalized coverage advice?

The legal framework remains unsettled. Current NAIC guidance holds that existing state insurance laws apply to AI systems just as they apply to human decisions, meaning the insurer or platform deploying the AI bears regulatory responsibility for the accuracy and fairness of any consumer-facing recommendation. A virtual insurance advisor AI can provide information and comparison data, but the suitability and fiduciary obligations that govern licensed human producers do not automatically attach to the AI itself.

3. How accurate are AI insurance recommendation systems compared to licensed brokers?

AI systems consistently outperform human agents on speed, multi-carrier data processing, and standardized personal lines quoting. However, independent analysis of major AI platforms in 2026 found that no system fully automates complex endorsement interpretation, all route those decisions to human reviewers. For complex commercial lines, Medicare Advantage selection, annuity products, and life insurance needs analysis, licensed human advisors retain a measurable accuracy and accountability advantage.

4. What happens if an AI chatbot gives me incorrect insurance advice?

Liability flows to the insurer or insurtech platform deploying the AI, not the AI system itself. Consumers who rely on AI-generated advice that proves to be inaccurate or unsuitable face a more complex legal remedy pathway than they would with a licensed broker, who carries E&O insurance and is subject to state insurance department complaint processes. The Air Canada chatbot case of 2024 established that organizations are legally responsible for their AI systems’ outputs. Consulting a licensed professional before binding significant coverage remains the safest consumer practice.

5. Do AI insurance tools have to disclose their conflicts of interest?

This is an area of active regulatory development. Licensed human producers in most states are subject to compensation disclosure requirements. AI advisory tools embedded in carrier websites present only that carrier’s products, a structural preference that may not be explicitly disclosed as a conflict. AI tools on aggregator platforms are somewhat more transparent, but commission transparency for AI-driven recommendations is not yet subject to the same explicit disclosure standards applied to licensed producers. The anticipated NAIC model law on third-party AI vendors may address this gap.

6. What is the suitability standard, and does it apply to AI insurance agents?

The suitability standard requires that any insurance recommendation be appropriate for the consumer’s stated needs, financial capacity, and coverage objectives. It is enforced through state insurance law and judicial precedent. In its current form, the suitability standard applies to licensed producers, and regulators hold the insurer responsible when an AI-driven recommendation violates it. However, the absence of a direct producer license for AI systems means enforcement mechanisms are less direct than they are in a dispute with a licensed individual.

7. Which U.S. states have the strongest regulations governing AI insurance advice?

As of April 2026, Colorado has enacted the most comprehensive framework, with its AI Act effective since February 1, 2026, requiring disclosure, bias prevention, and board-approved governance for AI systems used in insurance decisions. Approximately 24 states have adopted the NAIC’s AI Model Bulletin, which sets governance expectations without prescribing specific technical standards. States that have not adopted the Model Bulletin offer consumers fewer formal protections in AI-driven insurance advisory interactions.

8. Will AI replace licensed insurance agents by 2030?

Industry consensus in 2026 points strongly toward a hybrid model rather than full AI replacement of licensed producers. Agentic AI is expected to absorb high-volume, routine transactional work, quote generation, FNOL intake, policy renewal communications, and basic coverage comparisons. Complex advisory functions, claims advocacy, fiduciary-required product sales, and relationship management are expected to remain human-centered, with AI functioning as an analytical and efficiency layer rather than an autonomous replacement.

9. How can a consumer tell if an AI insurance tool is giving biased recommendations?

Detecting AI bias in insurance recommendations requires more transparency than most consumer-facing tools currently provide. The NAIC’s AI Model Bulletin calls for regular bias testing and audit procedures, but as of 2025, nearly one-third of health insurers had not implemented such testing. Consumers can ask whether an AI-driven platform has disclosed its model governance practices, whether it presents products from multiple carriers impartially, and whether a licensed professional has reviewed the recommendation methodology.

10. What is the best way to use AI insurance tools responsibly?

The most effective consumer approach in 2026 is to use AI-driven platforms for initial market comparison and quote gathering, particularly for standard personal lines products where coverage terms are well-defined and carrier pricing is the primary variable. For coverage decisions involving significant financial exposure, health-specific plan design, annuity or life products, or any product where a claims gap would produce a material loss, pairing the AI quoting experience with a consultation from a licensed professional provides the suitability and fiduciary protection that AI systems cannot independently supply. Neutral quote-comparison tools can be a practical starting point for gathering baseline market data before a professional review.